Off-Guardian | “We need a new approach to digital identity”, so say the authors of an “Agenda Article” for the World Economic Forum, published on the 28th of September.

Digital ID has been in the news a lot lately, obscured for the past week in the mist of the Israel-Hamas situation.

Just last week, Forbes Australia published it’s guide to what “Australians need to know” about digital IDs, and 9News reported that they could be in place as soon as next year.

Meanwhile, also in Australia, the world’s 21st largest bank is

changing its terms and conditions to allow it to “de-bank” customers.

The National Australian Bank’s “revised” terms and conditions go into force on November 1st and include, in clause 11: “NAB may close your account at any time at its discretion”.

The reasons NAB would consider enforcing clause 11 make for interesting reading [emphasis added]:

NAB can take a range of things into account when exercising its rights and discretions. These can include:

[…]

(e) NAB’s public statements, including those relating to protecting vulnerable persons, the environment or sustainability;

(f) community expectations and any impact on NAB’s reputation;

So – as of November 1st – NAB reserves the right to de-bank you if

you get cancelled, or say something they don’t approve of about climate

change or “vulnerable people”.

In the UK, just two days ago, it was reported the government is

planning to upload every passport photo in their records to a facial

recognition database.

Just yesterday India announced the launch of trial wholesale digital currency, and the South China Morning Post reported a new “hard-wallet” for SIM-based CBDC payments, a joint project between the Bank of China and Chinese telecommunications giants.

Back to Australia, where it was reported on October 12th that

Mastercard and the Reserve Bank of Australia had “successfully trialled”

the interoperability of CBDC systems, whilst ensuring that “the pilot CBDC can be held, used, and redeemed only by authorised parties“.

Mastercard’s report also notes that the benefits of CBDCs are “programmability, transparency, and compliance”.

amidwesterndoctor |•At the end of June, English Politician Nigel Farrage reported

that his bank accounts had been closed due to him sharing political

views that challenged the conventional narrative. Although his bank

originally denied deplatforming him for political reasons, an about-face

occurred and a few weeks later, the CEO resigned.

•On July 4th, a federal judge ruled

that the Biden administration was illegally violating the first

amendment by encouraging social media companies to censor anyone who

questioned the flawed COVID-19 narrative. Prior to this ruling, the

Biden administration was actively having critics of the pandemic policy

be censored and de-platformed. Since this ruling, as best as I can

tell, it is no longer as easy for them to de-platform political

opponents on social media.

Note: In May, a

moderately large regional bank collapsed and the Federal Government

decided to address the bank failure by having Chase bank to take the failed bank over.

This suggests that the Biden Administration is working hand in hand

with Chase and may be able to make requests in return for deals (like

the bank acquisition) it offered to Chase.

•On

July 6th, the FDA gave full approval to the Alzheimer’s drug that had

received a questionable backdoor approval in January (discussed below).

This approval was based on a 1795 person trial

(with 898 receiving the drug) where it was found the drug caused a

small decline in the rate of developing cognitive decline over 18 months

(based upon the results of a survey that could easily be prone to bias)

while at the same time 21.5% of those who received the drug experienced

brain bleeding and or brain swelling.

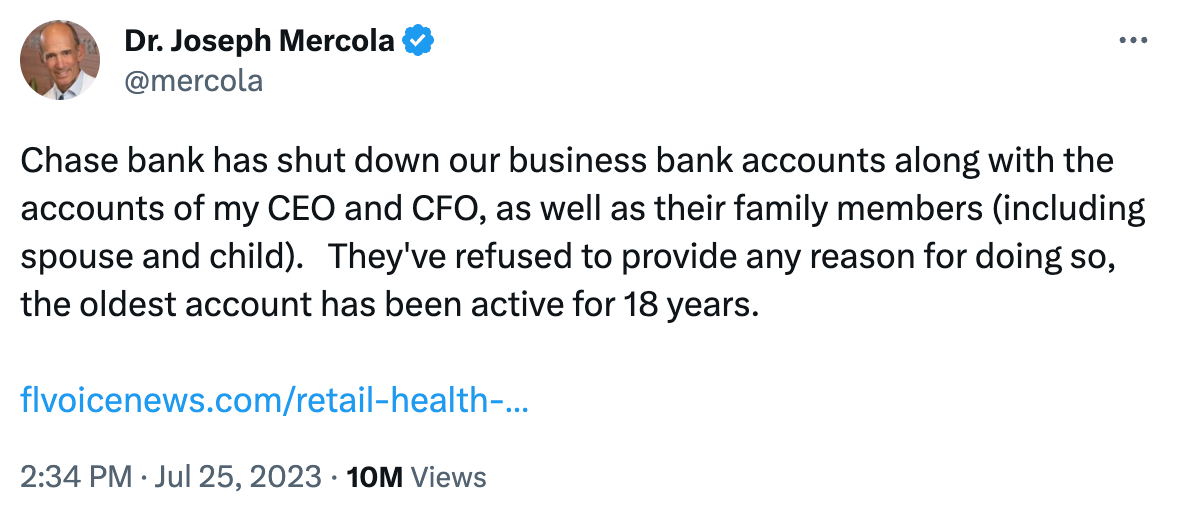

•On July 25th, Dr.

Mercola announced not only he, but also his employees and their families

had been abruptly deplatformed by Chase:

There are a lot of ways to interpret what happened. The most common

interpretation has been that debanking dissidents is fast becoming the

preferred way to suppress political opposition (e.g., do you remember

last year when Justin Trudaeu had Canada’s banks close all the bank

accounts of anyone who peacefully attended the Trucker protests against Canada’s vaccine mandates).

This

is likely being pushed forward since debanking is a relatively easy way

to create compliance in the population and there is an increasing risk

of widespread political rebellion against the bad policies (e.g., the

COVID-19 vaccine mandates) that have been pushed by governments around

the world. Typically, when policies like these are done, initially

small but visible tests are carried out (e.g., a lot of people can

clearly see what was done to the families of Dr. Mercola’s employees was

wrong) to gauge how the public will react to them and if that tyranny

can be normalized. Much of this in encapsulated by a famous poem I live my life by:

First they came for the socialists, and I did not speak out— Because I was not a socialist.

Then they came for the trade unionists, and I did not speak out— Because I was not a trade unionist.

Then they came for the Jews, and I did not speak out— Because I was not a Jew.

Then they came for me—and there was no one left to speak for me.

For

example, during Obama’s presidency, I watched easy to disparage groups

affiliated with the alt-right first be censored online and then be

deplatformed by Silicon Valley payment processors (e.g., Paypal). Many

of my left-wing friends who were worked in natural health applauded this

persecution and could not process why it might not be in their best

interests to promote it. That same censorship was then rolled out

against them (at which point no one stood up for them) and not to long

after that, against anyone who dissented against the COVID narrative.

Note:

Since the Federal Government was recently forced to back off from

overtly violating the First Amendment on social media, less overt ways

of suppressing speech are likely becoming a more and more needed tool

for those nonetheless wishing to do so.

However, while all of the above is likely true, there is another important facet to this entire story—antitrust violations.

After

the civil war, the US economy was taken over by a group of conniving

scoundrels who eventually came to be known as the Robber Barons. A key

approach they all shared was creating absolute monopolizations of their

respective industries, which allowed them to milk obscene amounts of

money as possible from everyone else.

Eventually Theodore Roosevelt put a stop to this through the 1890 Sherman Antitrust act,

and broke up their monopolies. I and many others believe that

Roosevelt was not entirely successful, because he caused the Robber

Barons to diversify into other areas (e.g., after Rockefeller had to

break up Standard Oil, he bought out the medical industry).

Since

Roosevelt’s time, efforts have been made to prevent big players from

monopolizing their respective industries (e.g., in the 1990s, Antitrust Lawsuits against Microsoft

revolved around Bill Gates having his Windows operating system not

allow competitors software on it), but they have not been as successful.

Since that time, Gates appears to have followed in Rockefeller’s

monopolizing footsteps and has gradually bought out the global health

industry through the leverage created by his foundation and its media

advertising dollars (which became obscene during COVID-19).

During

Obama’s presidency, we began to see a merger between Big Tech and Big

Pharma (as each invested in the other)—discussed further here and here.

This was then followed by a gradually increasing censorship of any

information online which challenged the pharmaceutical industry’s

narrative.

During COVID-19, this kicked into

overdrive. First, people were denied access to information about

numerous lifesaving therapies for COVID-19 (ultimately resulting in many

of them instead being forced to succumb to the remdesivir-ventilator

protocol). Following this, a blockade was enacted against any

information even hinting at the widespread harm emerging from the

COVID-19 vaccines, something most of us believe now caused even more

harm than denying the public access to early treatment options for

COVID-19. As you all know, many of the things Big Tech censored for

being “misinformation” (e.g., COVID-19’s origin from a lab) have since been proven true.

Many

have thus argued the Big Tech companies should be held accountable for

the harms that resulted from their monopolistic censorship. Although

their conduct is beyond egregious, it nonetheless makes a lot of sense

if you consider how many investments each industry had in the other and

the incentives they all had to monopolize the marketplace so they could

all make astronomical amounts of money off COVID-19.

NYTimes | For the second time in less than a decade, Elvira Nabiullina is steering Russia’s economy through treacherous waters.

In

2014, facing a collapsing ruble and soaring inflation after barely a

year as head of the Central Bank of Russia, Ms. Nabiullina forced the

institution into the modern era of economic policymaking by sharply

raising interest rates. The politically risky move slowed the economy,

tamed soaring prices and won her an international reputation as a tough

decision maker.

In the world of

central bankers, among technocrats tasked with keeping prices under

control and financial systems stable, Ms. Nabiullina became a rising

star for using orthodox policies to manage an unruly economy often

tethered to the price of oil. In 2015, she was named Central Bank

Governor of the Year by Euromoney magazine. Three years later, Christine

Lagarde, then the head of the International Monetary Fund, effused that

Ms. Nabiullina could make “central banking sing.”

Now

it falls to Ms. Nabiullina to steer Russia’s economy through a deep

recession, and to keep its financial system, cut off from much of the

rest of the world, intact. The challenge follows years she spent

strengthening Russia’s financial defenses against the kind of powerful

sanctions that have been wielded in response to President Vladimir V.

Putin’s geopolitical aggression.

She has guided the extraordinary rebound of Russia’s currency,

which lost a quarter of its value within days of the Feb. 24 invasion

of Ukraine. The central bank took aggressive measures to stop large sums

of money from leaving the country, arresting a panic in markets and

halting a potential run on the banking system.

In

late April, Russia’s Parliament confirmed Ms. Nabiullina, 58, for five

more years as chairwoman after Mr. Putin nominated her to serve a third

term.

“She’s an important beacon of stability for Russia’s financial system,” said

Elina Ribakova, the deputy chief economist of the Institute of

International Finance, an industry group in Washington. “Her

reappointment has symbolic value.”

Cleaning up the banks

Besides

her record on monetary policy, Ms. Nabiullina has drawn praise for

pursuing a thorough cleanup of the banking industry. In her first five

years at the bank, she revoked about 400 banking licenses — essentially

closing a third of Russia’s banks — in an effort to cull weak

institutions that were making what she termed “dubious transactions.”

It

was considered a brave crusade: In 2006, a central bank official who

had started a vigorous campaign to close banks suspected of money

laundering was assassinated.

“Fighting

corruption in the banking sector is a job for very courageous people,”

said Sergei Guriev, a Russian economist who left the country in 2013 and

is now a professor at Sciences Po in Paris. He called her program

flawed, though, because it was largely limited to private banks. This

created a moral hazard problem that left state-owned banks feeling

comfortable taking on lots of risk with the protection of the

government, he said.

Ms. Nabiullina’s

integrity has never been questioned, added Mr. Guriev, who said he had

known her for 15 years. “She’s never been suspected of any corruption.”

Before May 2020, M1 consists of (1)

currency outside the U.S. Treasury, Federal Reserve Banks, and the

vaults of depository institutions; (2) demand deposits at commercial

banks (excluding those amounts held by depository institutions, the U.S.

government, and foreign banks and official institutions) less cash

items in the process of collection and Federal Reserve float; and (3)

other checkable deposits (OCDs), consisting of negotiable order of

withdrawal, or NOW, and automatic transfer service, or ATS, accounts at

depository institutions, share draft accounts at credit unions, and

demand deposits at thrift institutions.

Beginning May 2020, M1

consists of (1) currency outside the U.S. Treasury, Federal Reserve

Banks, and the vaults of depository institutions; (2) demand deposits at

commercial banks (excluding those amounts held by depository

institutions, the U.S. government, and foreign banks and official

institutions) less cash items in the process of collection and Federal

Reserve float; and (3) other liquid deposits, consisting of OCDs and

savings deposits (including money market deposit accounts). Seasonally

adjusted M1 is constructed by summing currency, demand deposits, and

OCDs (before May 2020) or other liquid deposits (beginning May 2020),

each seasonally adjusted separately.

For more information on the

H.6 release changes and the regulatory amendment that led to the

creation of the other liquid deposits component and its inclusion in the

M1 monetary aggregate, see the H.6 announcements and Technical Q&As posted on December 17, 2020.

Suggested Citation:

Board of Governors of the Federal Reserve System (US),

M1 Money Stock [M1SL],

retrieved from FRED,

Federal Reserve Bank of St. Louis;

https://fred.stlouisfed.org/series/M1SL,

April 27, 2021.

Free To A Good Home

-

I know what gooning is same as I know what felching is but I don't care to

remind myself all that often about it. The Internet just keeps exposing the

ni...

If Free Will Is False, Destiny Is True

-

Free will is like God: perhaps dead, its absence having something to say

about morality (what Nietzsche meant by “Gott ist tot” was that the

Christian God ...

FREE BOOK: On Nonviolence

-

“Michael Barker’s interrogation of nonviolent protest tactics and regime

change is both timely and important. Drawing on cases ranging from American

democr...

Return of the Magi

-

Lately, the Holy Spirit is in the air. Emotional energy is swirling out of

the earth.I can feel it bubbling up, effervescing and evaporating around

us, s...

Covid-19 Preys Upon The Elderly And The Obese

-

sciencemag | This spring, after days of flulike symptoms and fever, a man

arrived at the emergency room at the University of Vermont Medical Center.

He ...

-

(Damn, has it been THAT long? I don't even know which prompts to use to

post this)

SeeNew

Can't get on your site because you've gone 'invite only'?

Man, ...

First Member of Chumph Cartel Goes to Jail

-

With the profligate racism of the Chumph Cartel, I don’t imagine any of

them convicted and jailed is going to do too much better than your run of

the mill ...