whatbitcoindid |Matthew Pines is the Director of Intelligence at the Krebs Stamos Group and a Fellow at the Bitcoin Policy Institute specializing in national security. In this interview, we discuss the growing sense that the US government may imminently disclose the existence of craft of non-human origin and that it actually possesses intact and partially intact examples of such craft.

- - - -

On July 26th, next Wednesday, the Republican-led House Oversight Committee will hold a hearing on unidentified anomalous phenomena (UAPs), a new term government agencies use for UFOs. Many believe that this change in nomenclature and the hearing is part of a process aimed at preparing the public for disclosure that the existence of non-human technology is real and that US government agencies and corporations may have retrieved craft of non-human origin.

Until recently, UAPs/UFOs were considered a fringe topic. Those in political circles and mainstream media organisations would publicly avoid the subject: it was officially ridiculed, and those who engaged in it risked career suicide. Now, it has suddenly become acceptable to seriously discuss the matter. On Monday (17th July), the White House itself stated UAPs are a "real issue" having "an impact" on the United States Air Force.

What changed?

Matthew Pines take us through the mechanisms of government bureaucracy in terms of official secrets: who gets clearances and the ‘need to know’. Matthew then takes us through the recent extraordinary whistleblower claims of a government coverup in relation to UAPs, why some within the government now feel enabled and compelled to come forward with extraordinary claims, and an effort to silence them.

It’s not hyperbolic to state that if such claims are publicly substantiated, it will be the biggest event in human history. It is telling that esteemed people who have close knowledge of this subject matter, including prominent politicians, high-ranking officials and qualified professionals, give credence to the UAP phenomenon. We wait with bated breath to see if these extraordinary claims are backed with extraordinary evidence.

TIMESTAMPS

00:00:00: Introductions 00:07:02: Matthew's background 00:14:13: Government structure of secrecy 00:24:41: Whistleblowing and potential scenarios 00:46:15: Credible explanations for ETs 00:54:52: Linking ETs to nuclear sites 01:04:04: Technological developments, and AI 01:10:10: Evidence and trusted reports 01:24:36: Normalising aliens 01:33:04: Implications for financial and political stability 01:45:01: Tangent to all things quantum 02:06:08: Interspecies communication 02:14:54: Timeline to truth 02:25:32: Final comments

WaPo | Sam Bankman-Fried, the 30-year-old wunderkind of cryptocurrency, spent

tens of millions of dollars over the past year trying to reshape how

Washington and the world think about finance.

The

crypto exchange he founded, FTX, had become an industry-dominating

business in just three years, valued at $32 billion as recently as

January. He amassed political clout in an even bigger hurry, emerging

from obscurity to become the second-biggest Democratic donor in the midterm elections.

By Friday, the money and the clout had disappeared: Bankman-Fried resigned from FTX, which then filed

for bankruptcy. And Bankman-Fried was left facing harrowing questions

about his role in the most catastrophic collapse the notoriously

volatile crypto industry has so far seen.

When

Bankman-Fried was just 28, he built a platform that offered investors

easy access to buying, selling and stashing bitcoin and other

cryptocurrencies. The offshore exchange allowed investors to place risky

bets not allowed in the United States, though it was easy enough

for American users to find workarounds; a U.S. affiliate offered

limited services. With a massive marketing push — including a flashy

Super Bowl ad and naming rights to the Miami Heat arena — he sought to

make crypto trading a mainstream pastime.

Meanwhile,

he was using his newfound political clout to sell Washington on a

regulatory regime that promised to work to his advantage. The contrasts

were glaring and never easily reconciled: As crypto’s self-appointed

ambassador to Washington, Bankman-Fried was pressing for federal

regulation even as he dodged U.S. oversight from his corporate

headquarters in the Bahamas.

The

executive acknowledged that FTX’s aggressive lobbying made him an

outlier in crypto. “Outside of us, there weren’t many people engaging,”

Bankman-Fried said in an interview last month with The Washington Post.

“I think that means we have to do a better job as an industry more

generally engaging.”

In March, he appeared at the House Democratic retreat in Philadelphia with his arm around House Financial Services Committee Chair Maxine Waters (D-Calif.). In April, he turned up

in the office of Caroline Pham, a Republican member of the Commodity

Futures Trading Commission, less than a week after she assumed the post,

along with Mark Wetjen, the former acting chair of the agency and now

Bankman-Fried’s top Washington adviser. Hill staffers say they regularly

spotted him around the Capitol, shuttling between meetings flanked by

Wetjen and Eliora Katz, who joined FTX this summer from the staff of the

Senate Banking Committee’s top Republican, Patrick J. Toomey (Pa.)

FT | “We do not like to get left behind when it comes to new technology,” she said.

The promise of cryptocurrencies as a wealth builder has been supercharged by celebrity endorsements, sponsorships and advertising.

Prominent black Americans including the musicians Jay-Z and Snoop Dogg, the boxer Floyd Mayweather, the actor Jamie Foxx and the film-maker Spike Lee have promoted crypto to their communities.

Lee appeared in commercials for crypto ATM operator Coin Cloud last year, saying that “old money is not going to pick us up; it pushes us down” and “systematically oppresses”, whereas digital assets are “positive, inclusive”.

Last month, Jay-Z announced a partnership with former Twitter chief executive Jack Dorsey to launch a “Bitcoin Academy” literacy programme in the Brooklyn public housing complex where he grew up.

Such celebrity endorsers have faced heavy criticism for getting paid to sell high-risk investments to people who may not have the resources to weather crypto’s volatility.

“Ninety-eight per cent of these cryptocurrencies were not designed to do anything other than extract money from people’s bank accounts,” said Najah Roberts, a former financial adviser and the founder of cryptocurrency education centre Crypto Blockchain Plug.

“This is not ‘get rich quick’,’’ Roberts added. “There are massive targeting ads that are targeting our community.”

Bellanton said it is not adverts but the prospect of financial freedom, a lack of the investment minimums common for mutual funds, and a feeling that the blockchain distributed ledger is more transparent than big banks that draws in first-time investors.

“The reason that minorities at a higher rate than others are adopting crypto is precisely because if you’re not already rich, it’s way cheaper to send [USD Coin, a stablecoin asset] than to send a wire,” said Brian Brooks, chief executive of blockchain company Bitfury, at the Aspen Ideas Festival last month. “It’s just cheaper.

The entire system is cheaper and faster. It doesn’t have all these entry barriers where you can only get it if you’re already rich.”

Despite the risk of losses, many black investors are staying invested in the market. Dennis McKinley, 41, has been buying the dip against the advice of his financial adviser. He said his crypto coins now constitute roughly 30 per cent of his overall portfolio, held alongside equities.

“Young black America is just now getting to a point where we have the amount of freedom to have the opportunity to invest in alternative strategies besides just real estate,” said McKinley, a small-business owner in Atlanta. “I think that it’s important to learn and get out there.”

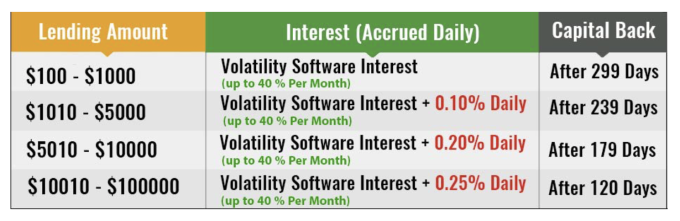

ibankcoin | Crypto currency Bitconnect (BCC) plunged from $321 to a tad over $35

today, a drop of more than 86% after regulators from state authorities

issued cease and desist letters for unauthorized sale of securities.

That’s right. Just because your shit is on the blockchain, that doesn’t

mean you get to solicit your fucking Ponzi scheme to people in America.

State regulators will have something to say about that.

Via the company’s website, as per the reasons for shutting down.

The reason for halt of lending and exchange platform has many reasons as follow:

The continuous bad press has made community members uneasy and created a lack of confidence in the platform.

We have received two Cease and Desist letters, one from the Texas State

Securities Board, and one from the North Carolina Secretary of State

Securities Division. These actions have become a hindrance for the legal

continuation of the platform.

Outside forces have performed DDos attacks on platform several times

and have made it clear that these will continue. These interruptions in

service have made the platform unstable and have created more panic

inside the community.

Price action.

What did Bitconnect do? They quite literally ran a Ponzi scheme. Look

at one of their brochures, promising investors 40% returns, PER MONTH.

Via Tech Crunch:

Many in the cryptocurrency community have openly accused

Bitconnnect of running a Ponzi scheme, including Ethereum founder

Vitalik Buterin.

The platform was powered by a token called BCC (not to be confused

with BCH, or Bitcoin Cash), which is essentially useless now that the

trading platform has shut down. In the last The token has plummeted more

than 80% to about $37, down from over $200 just a few hours ago.

If you aren’t familiar with the platform, Bitconnect was an

anonymously-run site where users could loan their cryptocurrency to the

company in exchange for outsized returns depending on how long the loan

was for. For example, a $10,000 loan for 180 days would purportedly give

you ~40% returns each month, with a .20% daily bonus.

Bitconnect also had a thriving multi-level referral feature, which

also made it somewhat akin to a pyramid scheme with thousands of social

media users trying to drive signups using their referral code.

The platform said it generated returns for users using Bitconnnect’s

trading bot and “volatility trading software”, which usually averaged

around 1% per day.

Of course profiting from market fluctuations and volatility is a

legitimate trading strategy, and one used by many hedge funds and

institutional traders. But Bitconnect’s promise (and payment) of

outsized and guaranteed returns led many to believe it was a ponzi

scheme that was paying out existing loan interest with newly pledged

loans.

The requirement of having BCC to participate in the lending program

led to a natural spike in demand (and price) of BCC. In less than a year

the currency went from being worth less than a dollar (with a market

cap in the millions) to a all-time high of ~$430.00 with a market cap

above $2.6B.

Lenders into the Bitconnect Exchange have revealed the company is

closing out accounts, issuing BCC in exchange for their dollars — which

is causing the price to plummet.

Bitconnect is officially closing up. They sent me

33 BCC for my $11k+ in loans. Worth $6600 and dropping by the second.

Their exchange is down so the only option is to send the BCC to an

external exchange.

journal-neo |Sadly, the Fed and

other central bankers lie. Raising interest rates is not to cure

inflation. It is to force a global reset in control over the world’s

assets, it’s wealth, whether real estate, farmland, commodity

production, industry, even water. The Fed knows very well that Inflation

is only beginning to rip across the global economy. What is unique is

that now Green Energy mandates across the industrial world are driving

this inflation crisis for the first time, something deliberately ignored

by Washington or Brussels or Berlin.

The global shortages

of fertilizers, soaring prices of natural gas, and grain supply losses

from global draught or exploding costs of fertilizers and fuel or the

war in Ukraine, guarantee that, at latest this September-October harvest

time, we will undergo a global additional food and energy price

explosion. Those shortages all are a result of deliberate policies.

Moreover, far worse

inflation is certain, due to the pathological insistence of the world’s

leading industrial economies led by the Biden Administration’s

anti-hydrocarbon agenda. That agenda is typified by the astonishing

nonsense of the US Energy Secretary stating, “buy E-autos instead” as

the answer to exploding gasoline prices.

Similarly, the

European Union has decided to phase out Russian oil and gas with no

viable substitute as its leading economy, Germany, moves to shut its

last nuclear reactor and close more coal plants. Germany and other EU

economies as a result will see power blackouts this winter and natural

gas prices will continue to soar. In the second week of June in Germany

gas prices rose another 60% alone. Both the Green-controlled German

government and the Green Agenda “Fit for 55” by the EU Commission

continue to push unreliable and costly wind and solar at the expense of

far cheaper and reliable hydrocarbons, insuring an unprecedented

energy-led inflation.

Fed has pulled the plug

With the 0.75% Fed

rate hike, largest in almost 30 years, and promise of more to come, the

US central bank has now guaranteed a collapse of not merely the US debt

bubble, but also much of the post-2008 global debt of $303 trillion.

Rising interest rates after almost 15 years mean collapsing bond values.

Bonds, not stocks, are the heart of the global financial system.

US mortgage rates

have now doubled in just 5 months to above 6%, and home sales were

already plunging before the latest rate hike. US corporations took on

record debt owing to the years of ultra-low rates. Some 70% of that debt

is rated just above “junk” status. That corporate non-financial debt

totaled $9 trillion in 2006. Today it exceeds $18 trillion. Now a large

number of those marginal companies will not be able to rollover the old

debt with new, and bankruptcies will follow in coming months. The

cosmetics giant Revlon just declared bankruptcy.

The

highly-speculative, unregulated Crypto market, led by Bitcoin, is

collapsing as investors realize there is no bailout there. Last November

the Crypto world had a $3 trillion valuation. Today it is less than

half, and with more collapse underway. Even before the latest Fed rate

hike the stock value of the US megabanks had lost some $300 billion. Now

with stock market further panic selling guaranteed as a global economic

collapse grows, those banks are pre-programmed for a new severe bank

crisis over the coming months.

As US economist Doug

Noland recently noted, “Today, there’s a massive “periphery” loaded with

“subprime” junk bonds, leveraged loans, buy-now-pay-later, auto, credit

card, housing, and solar securitizations, franchise loans, private

Credit, crypto Credit, DeFi, and on and on. A massive infrastructure has

evolved over this long cycle to spur consumption for tens of millions,

while financing thousands of uneconomic enterprises. The “periphery” has

become systemic like never before. And things have started to Break.”

The Federal

Government will now find its interest cost of carrying a record $30

trillion in Federal debt far more costly. Unlike the 1930s Great

Depression when Federal debt was near nothing, today the Government,

especially since the Biden budget measures, is at the limits. The US is

becoming a Third World economy. If the Fed no longer buys trillions of

US debt, who will? China? Japan? Not likely.

technologyreview | Libertarian attempts to create autonomous mini-civilizations go back at least to the 1960s, but crypto is reinvigorating this old dream with a fresh infusion of cash and hype.

For an idea

of what a corporate-run Bitcoin City might be like, look to a

burgeoning project called Próspera, supported by the Free Private Cities

Foundation in Honduras. While it’s not explicitly billed as a crypto

community, a heavy emphasis on the crypto industry and the backing of

heavyweight Bitcoin investors place Próspera in the same ideological

milieu—a fusion of crypto evangelism and libertarian credos.

Próspera (Spanish for “prosperous”) occupies a small enclave on the

Honduran island of Roatán. The developers have been handed the chance to

model a society from scratch, including its own health, education,

policing, and social security systems.

Honduras amended its

constitution in 2013 to allow the creation of special economic zones

managed by corporations and operating largely outside the country’s

legal and regulatory oversight. The resulting enclaves are known in

English as Zones of Economic Development and Employment (ZEDEs,

pronounced “zeh-dehs”).

The

decision was based on American economist Paul Romer’s proposal for

charter cities—a type of special economic zone in an existing state but

managed by another nation’s government. Considered one of his more outlandish ideas,

they reflect his theories about how to promote foreign investment and

alleviate inequality. Honduran ZEDEs are among the first tests of this

concept, though Romer has held talks with some other governments.

Romer

collaborated with the Honduran government at first, but they parted

ways following disagreements over how his idea was being implemented.

(Romer didn’t respond to a request for comment.)

Próspera, which

broke ground in 2020, plans to implement ultra-low taxes, outsource

services typically managed by the public sector, establish an

“arbitration center” in place of a court, and charge an annual fee for

citizenship (either physical or e-residency) that involves signing a

“social contract” the company hopes will discourage misbehavior.

When

I visited the site in February, a central office was one of the few

completed buildings. There was no private Próspera police force, but on

the front desk was a number for Bulldog Security International, a

private security company engaged by hotels on the island that consider

the local police force inadequate. A pair of two-story buildings housed

office workers. The rest was largely a construction site, although a

residential tower block is underway.

A rendering of the future Próspera shows apartments that appear to

take inspiration from the shells of the island’s indigenous conch—soft

curves in pearly coral, cream, and glass. A strip of white sand

separates the apartment block from the gentle lap of the Caribbean Sea.

The

businesses most likely to be drawn here are those keen to escape

regulation in their own countries—Próspera’s chief of staff, Trey Goff,

highlights medical innovation, health tourism, and just about every

facet of the cryptocurrency industry.

“There’s an automatic

degree of overlap with the crypto industry and what we’re doing,” he

says. “Because they see themselves as at the forefront of financial

innovation, and we want to enable that.”

globeandmail | The Ontario government

says it has successfully petitioned a court to freeze access to millions

of dollars donated through online fundraising platform GiveSendGo to

the convoy protesting COVID-19 restrictions in Ottawa and at several border crossings.

The

province obtained an order from the Superior Court of Justice that

prohibits anyone from distributing donations made through the website’s

“Freedom Convoy 2022″ and “Adopt-a-Trucker” campaign pages, said a

spokeswoman for Premier Doug Ford.

Ivana

Yelich said the order binding “any and all parties with possession or

control over these donations” was issued Thursday afternoon. She cited a

section of the Criminal Code that allows the attorney general to apply

for a restraint order against any “offence-related property.”

Donors

initially raised more than $10-million through GoFundMe, which

announced last Friday it was pulling the plug on the campaign and that

the money would be refunded. The site said it initially believed the

demonstration was going to be peaceful, but withdrew its support after

police and local leaders raised concerns it had become an “occupation.”

Convoy

organizers quickly set up new campaigns on Christian fundraising site

GiveSendGo. As of Thursday, “Freedom Convoy 2022″ had raised

$US8.4-million and “Adopt-a-Trucker” had amassed more than $686,000.

GiveSendGo posted a statement on Twitter Thursday night about its “Freedom Convoy” campaign.

“Know this! Canada has absolutely ZERO jurisdiction over how we manage our funds here at GiveSendGo,” it said.

“All

funds for EVERY campaign on GiveSendGo flow directly to the recipients

of those campaigns, not least of which is The Freedom Convoy campaign.”

Organizers

have also touted the cryptocurrency Bitcoin as another way to generate

funds for protesters and avoid other potential fundraising shutdowns,

including during a news conference that was livestreamed to supporters

on Wednesday.

Ontario’s

move to freeze access to the donations comes the same day as an

all-party House of Commons committee of MPs heard testimony from deputy

directors of Canada’s financial intelligence hub about how it doesn’t

cover crowdfunding sites like GoFundMe.

The more employees of large media corporations attack Joe Rogan, the more his audience grows. The two individuals with the largest audiences happen to be the two people most hated by corporate media because they can't be controlled or ordered around:https://t.co/kjgUQRwWIs

zerohedge | When the last hour of the podcast was coming to its conclusion as I

was finishing an 8 mile run, a thought dawned on me: this interview with

Malone is now officially out there and, no matter how much anyone tries to censor it, it can’t be taken back.

As we all know, nowadays when you make it on JRE, you’ve officially “made it”.

Putting

aside the obvious irony of Twitter attempting to ban somebody and the

person in question going viral as a result, I also thought about how,

despite the fact that Malone’s opinions put him at odds with the

mainstream media (who would never dare to have him on), Joe Rogan

launched him past the usual media suspects and into the real “mainstream”.

I then thought to myself that in 2022, the mainstream media as we know it today (CNN, MSNBC, ABC, CBS, etc.) is going to be forced to change its narrative on Covid.

“It’ll never happen,” you’re thinking to yourself, right? Let me explain.

* * *

The idea of the media being forced to change its tune on Covid is something I touched upon a couple of days ago when I wrote about the Omicron variant and how the media is creating a mass hysteria mountain out of a mole hill.

But

after listening to Dr. Robert Malone‘s well reasoned arguments,

delivered for three straight hours, concisely and calmly, it became

clear to me that the entire mainstream media machine could wind up

falling at the hands of content creators like Joe Rogan.

It’s an interesting little piece of game theory, when you think about it.

Rogan generates so many views and has grown so quickly - strictly because he

allows open dialogue, civil discourse and approaches things with honest

intent – that there is no financial incentive to de-platform him. Ever

notice how YouTube apparently had no problem taking down Rogan’s interview with Malone, but hasn’t banned Rogan’s channel from the site yet?

thecorrespondent | It seems that blockchain sounds best in a PowerPoint slide. Most blockchain projects don’t make it past a press release, an inventory by Bloomberg showed. The Honduran land registry was going to use blockchain. That plan has been shelved. The Nasdaq was also going to do something with blockchain. Not happening. The Dutch Central Bank then? Nope. Out of over 86,000 blockchain projects that had been launched, 92% had been abandoned by the end of 2017, according to consultancy firm Deloitte.

Why are they deciding to stop? Enlightened – and thus former – blockchain developer Mark van Cuijk explained: “You could also use a forklift to put a six-pack of beer on your kitchen counter. But it’s just not very efficient.”

I’ll list a few of the problems. Firstly: the technology is at loggerheads with European privacy legislation, specifically the right to be forgotten. Once something is in the blockchain, it cannot be removed. For instance, hundreds of links to child abuse material and revenge porn were placed in the bitcoin blockchain by malicious users.

It’s impossible to remove those.

Also, in a blockchain you aren’t anonymous, but “pseudonymous”: your identity is linked to a number, and if someone can link your name to that number, you’re screwed. Everything you got up to on that blockchain is visible to everyone.

The presumed hackers of Hillary Clinton’s email were caught, for instance, because their identity could be linked to bitcoin transactions. A number of researchers from Qatar University were able to ascertain the identities of tens of thousands of bitcoin users fairly easily through social networking sites. Other researchers showed how you can de-anonymise many more people through trackers on shopping websites.

The fact that no one is in charge and nothing can be modified also means that mistakes cannot be corrected. A bank can reverse a payment request. This is impossible for bitcoin and other cryptocurrencies. So anything that has been stolen will stay stolen. There is a continuous stream of hackers targeting bitcoin exchanges and users, and fraudsters launching investment vehicles that are in fact pyramid schemes. According to estimates, nearly 15% of all bitcoin has been stolen at some point. And it isn’t even 10 years old yet.

On Friday of last week, the

Juneteenth holiday, a leak-focused activist group known as Distributed

Denial of Secrets published a 269-gigabyte collection of police data

that includes emails, audio, video, and intelligence documents, with

more than a million files in total. DDOSecrets founder Emma Best tells

WIRED that the hacked files came from Anonymous—or at least a source

self-representing as part of that group, given that under Anonymous'

loose, leaderless structure anyone can declare themselves a member. Over

the weekend, supporters of DDOSecrets, Anonymous, and protesters

worldwide began digging through the files to pull out frank internal

memos about police efforts to track the activities of protesters. The

documents also reveal how law enforcement has described groups like the

antifascist movement Antifa.

"It's the largest published hack of

American law enforcement agencies," Emma Best, cofounder of DDOSecrets,

wrote in a series of text messages. "It provides the closest inside look

at the state, local, and federal agencies tasked with protecting the

public, including [the] government response to COVID and the BLM

protests."

The Hack

The

massive internal data trove that DDOSecrets published was originally

taken from a web development firm called Netsential, according to a law

enforcement memo obtained by Kreb On Security.

That memo, issued by the National Fusion Center Association, says that

much of the data belonged to law enforcement "fusion centers" across the

US that act as information-sharing hubs for federal, state, and local

agencies. Netsential did not immediately respond to a request for

comment.

Best declined to comment on whether the information was

taken from Netsential, but noted that "some Twitter users accurately

pointed out that a lot of the data corresponded to Netsential systems."

As for their source, Best would say only that the person

self-represented as "capital A Anonymous," but added cryptically that

"people may wind up seeing a familiar name down the line."

DDOSecrets

has published the files in a searchable format on its website, and

supporters quickly created the #blueleaks hashtag to collect their

findings from the hacked files on social media. Some of the initial

discoveries among the documents showed, for instance, that the FBI

monitored the social accounts of protesters and sent alerts to local law

enforcement about anti-police messages. Other documents detail the FBI

tracking bitcoin donations to protest groups, and internal memos warning

that white supremacist groups have posed as Antifa to incite violence.

Medium |Last

year, I got invited to a super-deluxe private resort to deliver a

keynote speech to what I assumed would be a hundred or so investment

bankers. It was by far the largest fee I had ever been offered for a

talk — about half my annual professor’s salary — all to deliver some

insight on the subject of “the future of technology.”

I’ve

never liked talking about the future. The Q&A sessions always end

up more like parlor games, where I’m asked to opine on the latest

technology buzzwords as if they were ticker symbols for potential

investments: blockchain, 3D printing, CRISPR. The audiences are rarely

interested in learning about these technologies or their potential

impacts beyond the binary choice of whether or not to invest in them.

But money talks, so I took the gig.

After

I arrived, I was ushered into what I thought was the green room. But

instead of being wired with a microphone or taken to a stage, I just sat

there at a plain round table as my audience was brought to me: five

super-wealthy guys — yes, all men — from the upper echelon of the hedge

fund world. After a bit of small talk, I realized they had no interest

in the information I had prepared about the future of technology. They

had come with questions of their own.

They

started out innocuously enough. Ethereum or bitcoin? Is quantum

computing a real thing? Slowly but surely, however, they edged into

their real topics of concern.

Which

region will be less impacted by the coming climate crisis: New Zealand

or Alaska? Is Google really building Ray Kurzweil a home for his brain,

and will his consciousness live through the transition, or will it die

and be reborn as a whole new one? Finally, the CEO of a brokerage house

explained that he had nearly completed building his own underground

bunker system and asked, “How do I maintain authority over my security

force after the event?”

democracynow | Look, Amy, in slaves-owning societies or in the Middle Ages, we had

production. People worked, toiled the land. Then we had distribution.

The lord would send his henchmen in, his sheriff, to take his cut. So

you had distribution—production, distribution. The lord’s cut would then

be sold in markets. He would get money out of it, and then you would

have finance. So we had production, distribution, finance.

With capitalism, we had the reversal of that. First you’d get the

debt, to set up the—you know, to employ people. So you have finance,

then distribution, and the last thing that happens is production. So,

debt is central to capitalism. Now, that means one thing: The banker,

the financier, has an exorbitant privilege. He’s like the sorcerer who

has the capacity to push his hand through the time line, snatch value

from the future, that has not been produced yet, and bring it in to the

present to help orchestrate the production that will create the value

that will be repaid in the future. But, effectively, you’re creating a

class of people, the financiers, who then have complete control over

society. And they can keep doing this a lot more, until the present can

no longer repay the future, and there is a huge crash. And then what

happens? Because they have this privileged position, they can make you

and me, President Obama, whoever, Larry Summers, bail them out. So, they

win if their bets succeed, and they win if their bets lose. What kind

of political economy is this, when you have one class of people who win,

whatever they do, and everybody else loses, whatever they do?

AMYGOODMAN: Is this what you refer to the black magic of banking?

YANISVAROUFAKIS: That’s exactly right.

AMYGOODMAN: And so, what’s the cure for this?

YANISVAROUFAKIS: Well, the cure of this is, effectively, to do that which FDR did in the 1930s.

AMYGOODMAN: President Roosevelt.

YANISVAROUFAKIS:

President Roosevelt—to put the financial genie back in the bottle. Make

banking boring again. Put huge constraints upon them. Nationalize the

banks and turn them into institutions for public purpose. And if

even—you don’t necessarily need to nationalize, as long as you really

keep them under strict control. Remember Bretton Woods, which designed

the golden era of capitalism. Bretton Woods was a conference in 1944,

and there 120 different countries agreed on the system which saw, in the

1950s and 1960s, the longest period of steady growth, with shrinking

inequality and low unemployment and low inflation. FDR

had one condition slapped onto membership of that Bretton Woods

Conference. Do you know what it was? No banker was allowed in the

Washington—the Mount Washington Hotel. So you had a monetary and

financial system that was designed in the absence of bankers. That’s

what we should do again.

AMYGOODMAN: What is apolitical money?

YANISVAROUFAKIS:

In this country, you have a lot of people, good people, who are fed up

with politicians, who are fed up with the Fed, and who believe that—they

believe in true money, in honest money, that money should be somehow

independent of the political process. Remember the gold standard? They

still hanker after the gold standard. They would like the quantity of

dollars printed to be linked to the quantity of gold that the Fed owns,

so that there would be no political influence of the quantity of money,

because they fear that—they fear the government will print too much

money, and there will be inflation, and the value of money will be

effectively eaten away—the gold bugs, as you call them in this country.

Bitcoin—Bitcoin is a digital form of the gold standard. And so, the

backlash against political control—

AMYGOODMAN: The Bitcoin folks are moving into Puerto Rico right now, has been devastated by Maria.

YANISVAROUFAKIS: Of course it’s been devastated. But the solution is not Bitcoin.

AMYGOODMAN: But they’re moving in fast.

YANISVAROUFAKIS:

Yes, but it’s—you know, it’s just a bubble. It will burst. And the

reason is, however much we loathe the political process because it is

controlled by oligarchs and by the same old financiers who are behind

the politicians who are bailing them out whenever the finance is

needed—however much we dislike that, there is no alternative to

political money. Why? Because the quantity of money must be in sync with

the quantity of output of goods and services. If those two go out of

sync, you have deflationary bouts. You have to—that will lead to

depression. So, to put it very bluntly and simply, the quantity of money

must be decided democratically. At the moment, it’s not being decided

democratically. It’s decided politically, but oligarchically. The

solution is not to take it and tie it to some algorithm.

AMYGOODMAN:

In the United States, you—in the United States, you only refer to

oligarchy when you’re talking about Russia, the oligarchs. But

billionaire businessmen in the United States, you do not refer to as

oligarchs.

YANISVAROUFAKIS:

But the United States of America is the prime oligarchy. The difference

between the United States of America and Russia is that the United

States is a more successful oligarchy. But it is an oligarchy

nevertheless.

AMYGOODMAN: Explain.

YANISVAROUFAKIS:

Well, think of 2008. President Obama is sworn in on a wave of

expectation by the victims of the financiers. And what does he do? First

thing he does is he appoints Larry Summers and Tim Geithner, the very

same people who had actually unshackled the financiers in the late

1990s, allowing them to do everything that brought so much discontent to

the very same people who then entrusted President Obama. President

Obama, very soon after that, lost his credibility with those people, and

the result is Donald Trump. That’s an oligarchy.

AMYGOODMAN:

And so, why is Donald Trump so fiercely opposed to President Obama—is

it just racial?—given that he laid the groundwork for the oligarchs, for

people like Donald Trump, if, in fact, he does have money?

YANISVAROUFAKIS:

Well, the ruling class has a fantastic capacity, like the working

class, to be divided. Donald Trump was never in the pocket of Wall

Street. He used Wall Street. He used Deutsche Bank. He used all the

people he dislikes, in order to keep, effectively, bankrupting his

companies and profiting from it. So he’s really very good at that. But

he was never very successful as a businessman, certainly not as

successful as Goldman Sachs or JPMorgan. And he was always on the

margins of the capitalist order of things in the United States. He

understood that in order for him to gain more power, more—both

discursively and politically and economically, he had to ride the wave

of discontent against Obama. And he did this magnificently. And the

Democrats let him. The Democrats brought their own distress and failure

upon themselves.

AMYGOODMAN:

So I want to talk about the rise of the right, but go back to World War

II—actually, between World War I and World War II in Germany. How do

you see the growth of the support for Hitler and how he took power in

Germany, going back to World War I and the devastation of Germany?

YANISVAROUFAKIS:

The combination—the combination of a humiliated populace. The

humiliation is very important, Amy. When you humiliate a whole people in

the middle of a great depression, great economic crisis, you have a

political crisis. So the political center implodes, which is what

happened with the Weimar Republic, and then all sorts of political

monsters ride up—rise up from that. We saw this in the 1920s, the 1930s,

in the midwar period in Germany. But we saw it in—we see it in Greece

today, after—do you know we have a Nazi party in Greek Parliament—in the

country that, along with Yugoslavia, fought tooth and nail against

Nazism in the 1940s. We had a magnificent resistance movement against

Nazism. In that country now, the third-largest party is a—not a neo-Nazi

party, fully old-fashioned Nazi party.

AMYGOODMAN: And this came into the Parliament when?

YANISVAROUFAKIS:

They came into Parliament in 2012, at the time of a humiliated public

in the clasp of a great depression, just like in Germany in the 1930s.

But allow me to make a point, because there is a great

misunderstanding about Germany of the midwar period. Usually people say,

“Oh, it was hyperinflation. It was the fact that prices were rising

exponentially that brought Hitler to power.” Not true. It is true that

hyperinflation depleted the middle class, effectively destroyed the

middle class’s savings and shook the system and made the Weimar Republic

extremely fragile and ready for the taking. But if you look at the

electoral performance of the Nazi Party in Germany, there is a direct

correlation, not with inflation, but with deflation. You had Chancellor

Brüning, who in 1930 decided to slam the brakes on the economy and to

use large doses of austerity in order to make inflation go away—a bit

like Paul Volcker when he pushed interest rates up in the early '80s,

remember, to 20-something percent—and a lot more fiscal austerity, not

just monetary austerity. It was at that point when prices started

falling in Germany. Prices started falling, and unemployment ballooned.

And that is when you have a major jump in the support for Nazis.

Deflation breeds fascism. And that is something that we've got to

remember. And I’m making this point because, unfortunately, the European

Union’s economic policies today are producing deflationary forces that

are being exported to the United States and to China. And that does not

augur well for progressive international politics.

AMYGOODMAN:

So talk now about the far right in Europe and also in the United

States. But in Europe, you’re talking about Poland, you’re talking about

Hungary. You’ve got Golden Dawn, not to mention the Nazi party, in

Greece.

YANISVAROUFAKIS: Oh, that’s the Golden—the Golden Dawn is a Nazi party. That’s the Nazi party I was referring to.

medium |Blockchain

is not only crappy technology but a bad vision for the future. Its

failure to achieve adoption to date is because systems built on trust,

norms, and institutions inherently function better than the type of

no-need-for-trusted-parties systems blockchain envisions. That’s

permanent: no matter how much blockchain improves it is still headed in

the wrong direction.

Let’s start with this: Venmo is a free service to transfer dollars, and bitcoin transfers are not free. Yet after I wrote an article last December saying bitcoin had no use, someone responded that Venmo and Paypal are raking in consumers’ money and people should switch to bitcoin.

What

a surreal contrast between blockchain’s non-usefulness/non-adoption and

the conviction of its believers! It’s so entirely evident that this

person didn’t become a bitcoin enthusiast because they were looking for a

convenient, free way to transfer money from one person to another and

discovered bitcoin. In fact, I would assert that there is no single person in existence

who had a problem they wanted to solve, discovered that an available

blockchain solution was the best way to solve it, and therefore became a

blockchain enthusiast.

There is no single person in existence

who had a problem they wanted to solve, discovered that an available

blockchain solution was the best way to solve it, and therefore became a

blockchain enthusiast.

The number of retailers accepting cryptocurrency as a form of payment is declining, and its biggest corporate boosters like IBM, NASDAQ, Fidelity, Swift and Walmart have gone long on press but short on actual rollout. Even the most prominent blockchain company, Ripple, doesn’t use blockchain in its product. You read that right: the company Ripple decided the best way to move money across international borders was to not use Ripples.

A blockchain is a literal technology, not a metaphor

Why all the enthusiasm for something so useless in practice?

People have made a number of implausible claims about the future of blockchain—like that you should use it for AI

in place of the type of behavior-tracking that google and facebook do,

for example. This is based on a misunderstanding of what a blockchain

is. A blockchain isn’t an ethereal thing out there in the universe that

you can “put” things into, it’s a specific data structure: a linear

transaction log, typically replicated by computers whose owners (called

miners) are rewarded for logging new transactions.

themaven | I completely agree with much of what you wrote here. I’d like to point out a couple things:

First, in regards

to “There is no single person in existence who had a problem they wanted

to solve, discovered that an available blockchain solution was the best

way to solve it, and therefore became a blockchain enthusiast.” There

is in fact at least one such person: me. In 2010 I was looking for a

payment system which did not have any possibility for chargebacks. It

turns out that bitcoin is GREAT for that, and I became a blockchain

enthusiast as a result.

The ugly truth

about blockchain is that it is immensely useful, but only when you are

in some way trying to circumvent an authority of some sort. In my case, I

wanted to take payments for digital goods without losing any to

chargebacks. It’s also great for sending money to Venezuela

(circumventing the authority of the government of Venezuela, which would

really rather you not). It’s great for raising money for projects (ICOs

are really about circumventing various regulatory authorities who make

that difficult). It’s great for buying drugs, taking payment for

ransomware, and any number of terrible illegal things related to human

trafficking, money laundering, etc.

Frankly, the day

that significant trading of derivatives (gold futures, oil futures,

options, etc) starts happening on blockchain, I expect a bubble that

will make previous crypto bubbles look tiny in comparison. This is not

because blockchain is an easier way to trade these contracts! It is

because some percentage of rich traders would like to do anonymous

trading and avoid pesky laws about paying taxes on trading profits and

not doing insider trading.

I sum it up like

this: are you trying to do something with money that requires avoiding

an authority somewhere? If not, there is a better technical solution

than blockchain. That does NOT mean that what you are doing is illegal

for you (it’s perfectly legal for me to send money to Venezuela). It

just means that some authority somewhere doesn’t like what you are

doing.

Blockchain is

inherently in opposition to governmental control of the world of

finance. The only reason governments aren’t more antagonistic towards

blockchain is that they don’t truly understand how dangerous it is. I

wrote at length about this back in 2013 in an article called “Bitcoin’s

Dystopian Future”:

It took a minute to figure out that TOR is the antithesis of what it claims to be - and is in fact nothing other than a surveillance honeypot. Fool me once, shame on you. Fool me twice, shame on me....,

anonhq | To some Bitcoin is the Free Market’s answer to crony capitalism, communism, the endless inflation of fiat currencies and all that is wrong with the world. To others, it is a worthless digital creation – numbers on a screen with no backing, a bubble with no value beyond what arbitrarily imagined number a savvy Crypto “Expert” would tell you.

In between, you have those that view Bitcoin as a Ponzi scheme – but one worth cashing in on while the getting is good; those who use it as a deflationary store of wealth, akin to a prized Picasso but more liquid; and those who see the rise of other cryptos that could do what Bitcoin does – but better, and dethrone Bitcoin with a one true cryptocurrency to break the banks.

There is one last school of thought, the conspiracy theorist of conspiracy theories so to speak; What if Bitcoin is, in fact, a creation of the NSA?

It would seem that Satoshi cannot claim credit for being the first to come up with the idea; a document titled “How to make a mint: The cryptography of anonymous electronic cash” was written in 1997 and authored by none other than Laurie Law, Susan Sabett and Jerry Solinas of the “National Security Agency Office of Information Security Research and Technology”.

Satoshi mined the genesis block of the bitcoin blockchain in January 2009, some 12 years after the paper was written. Interestingly, Tatsuaki Okamoto is cited frequently in the paper, though beyond the apparent similarity to Satoshi Nakamoto it probably doesn’t mean anything.

The paper describes signature authentication techniques, methods to prevent the counterfeiting of cryptocurrencies via transaction authentication, and mentions terminology common to current cryptocurrencies such as “tokens”, “coins”, “Secure Hashing” and “digital signatures” years before Bitcoin.

It should be noted that the paper appears to be directed towards banks, and that it does not include mining or a p2p blockchain authentication system, but given the decade between conceptualization and implementation these features may have evolved. If nothing else Satoshi must have gotten some inspiration from the paper.

The NSA also invented the hash function that Bitcoin is predicated on, SHA-256. Thanks to Edward Snowden’s leaks, we also know that the NSA has inserted backdoors into its encryption standards before. With so many poring over the open-source code though, it is unknown if the NSA could really get away with a backdoor.If the NSA came up with the idea years before Satoshi did, and Bitcoin is dependent on an NSA hash, the theory goes that at the very least the NSA has some stake/ control over/ ulterior motive regarding Bitcoin. On the other hand, the US government created TOR and the Internet; if the NSA had a finger in its creation, perhaps this is another experiment that “got away” from the government…

NYTimes | Worried about someone hacking the next election? Bothered by the way Facebook and Equifax coughed up your personal information?

The technology industry has an answer called the blockchain — even for the problems the industry helped to create.

The first blockchain was created in 2009 as a new kind of database for the virtual currency Bitcoin, where all transactions could be stored without any banks or governments involved.

Now, countless entrepreneurs, companies and governments are looking to use similar databases — often independent of Bitcoin — to solve some of the most intractable issues facing society.

“People feel the need to move away from something like Facebook and toward something that allows them to have ownership of their own data,” said Ryan Shea, a co-founder of Blockstack, a New York company working with blockchain technology.

The creator of the World Wide Web, Tim Berners-Lee, has said the blockchain could help reduce the big internet companies’ influence and return the web to his original vision. But he has also warned that it could come with some of the same problems as the web.

Blockchain allows information to be stored and exchanged by a network of computers without any central authority. In theory, this egalitarian arrangement also makes it harder for data to be altered or hacked.

Investors, for one, see potential. While the price of Bitcoin and other virtual currencies have plummeted this year, investment in other blockchain projects has remained strong. In the first three months of 2018, venture capitalists put half a billion dollars into 75 blockchain projects, more than double what they raised in the last quarter of 2017, according to data from Pitchbook.

Most of the projects have not gotten beyond pilot testing, and many are aimed at transforming mundane corporate tasks like financial trading and accounting. But some experiments promise to transform fundamental things, like the way we vote and the way we interact online.

“There is just so much it can do,” said Bradley Tusk, a former campaign manager for Michael R. Bloomberg, the former mayor of New York, who has recently thrown his weight behind several blockchain projects. “I love the fact that you can transmit data, information and choices in a way that is really hard to hack — really hard to disrupt and that can be really efficient.”

Mr. Tusk, the founder of Tusk Strategies, is an investor in some large virtual currency companies. He has also supported efforts aimed at getting governments to move voting online to blockchain-based systems. Mr. Tusk argues that blockchains could make reliable online voting possible because the votes could be recorded in a tamper-proof way.

“Everything is moving toward people saying, ‘I want all the benefits of the internet, but I want to protect my privacy and my security,’” he said. “The only thing I know that can reconcile those things is the blockchain.”

theroot | Hey, man, we didn’t do an explainer last week, but I really need to

talk to you about this Boyce Watkins thing that is bubbling on woke

Twitter.

Sure! Earlier this week, a video of a screenshot of what

seems to be an online conference call began circumnavigating the

inboxes of the woke black internet. The video shows two men having a

conversation about Boyce Watkins, Ph.D., and his ...

Wait, bruh. Who the hell is Boyce Watkins?

Watkins

is the less charismatic Umar Johnson of black financial independence

and wealth. His Black Business School is a virtual version of Umar

Johnson’s Kente Cloth Hogwarts for Black Boy Magic, except, of course,

that Watkins’ really exists. While Watkins’ educational products seem to

be the equivalent of freshman-level community college business-theory

courses with a little Creflo Dollar sprinkled in, remember, the BBS is

100 percent black. (Remember this point. It is important.)

If I were still using the term “Hotep” as a pejorative—which I am not—I

would call Watkins a level 3, low-ranking Ankhologist, perfect for

easing black people who are not particularly educated or experienced in

Watkins’ area of kente-clothians. He is a perfect conduit conning people

into becoming practitioners of entry-level dashikinomics. Plus,

Watkins’ school is 100 percent black, meaning that you don’t have to

worry about any Caucasian shenanigans creeping into play.

OK, now back to the video.

So the videos show Charles Wu bragging about JARVIS and the Digital Underground and how ...

Slow

down! Who is Charles Wu? Is Jarvis one of the lesser-known members of

the Wu-Tang Clan? And what does Shock G and Humpty have to do with any

of this?

Sorry. It’s just that there’s a lot to cover.

The

Digital Underground, or “the D.U.,” as it is called, is not a reference

to the ’90s rap group. It is a course in Watkins’ Black Business School.

For $2,999 (or the low price of $499 per month),

instead of reading Wikipedia and doing a couple of Google searches, you

can have Watkins teach you everything he knows about altcoin,

blockchain and bitcoin (which, coincidentally, seems to not be much. But

for those who don’t know anything, it seems like a lot. After

all, his name has “Dr.” right in it!) Plus, you can trust Watkins. He’s

leading black people toward their “Financial Juneteenth” (his actual

term). He’s a solid dude.

Oh, did I mention the school was 100 percent black?

Strategic-Culture | It

is probably too early for the common man to understand what is

happening, but in fact the dollar is depreciating in relation to some

more tangible assets. But gold continues to be corralled by parallel financial mechanisms and

other financial instruments created for the sole purpose of

manipulating the financial markets on which the common man depends in

search of modest gains. As with others, the gold market suffers from the

combine power of the US dollar, centralized financial institutions and

market manipulation. Entities such as the FED (and their owners),

criminally colluding and working with private banks, hedge funds,

rating agencies and audit companies, have made immense wealth by driving

the world into a debt scam that has stripped normal citizens of their

future.

What

is happening in the cryptocurrency markets in not only occurring in

parallel with the spread of the Internet, smartphones and the increasing

ability to operate in the digital world, but is also seen as a safe

haven from centralized financial regulators and central banks; in other

words, from the dollar and fiat currencies in general. Whether bitcoin

will prove to be a wise long-term investment is yet to be seen, but the

concept of cryptocurrencies is here to stay. The technology behind the

idea, the blockchain, is a definitive model for decentralized economic

transactions without any intermediary that can manipulate and distort

the market at will. It is the antidote to the debt virus that is killing

our society and spreading chaos around the world.

Washington

is now left to deal with the consequences of its demented actions

against its geopolitical adversaries. The decision to remove Iran from

the SWIFT system, and the ongoing economic war against Russia and

Venezuela, have pushed the People's Republic of China to obviate any

direct attacks on its financial system by creating an alternative

economic system. The goal is to warn the United States and her allies

that an economic alternative exists and is already operational, ready to

be opposed to the Euro-American system if necessary. Washington does

not seem to want to renounce the role of manipulator and ruler of world

speculative finance, and the obvious result of this is the creation of a

financial system that is slowly working against the current one. Lack

of anonymity and the centrality of systems seem to be the two

fundamental elements of the current financial system that orbits around

London and Washington. An anonymous, decentralized and technologically

reliable system could be exactly what Washington's geopolitical

adversaries have been looking for to end the US-Dollar hegemony.

ibankcoin | Crypto currency Bitconnect (BCC) plunged from $321 to a tad over $35

today, a drop of more than 86% after regulators from state authorities

issued cease and desist letters for unauthorized sale of securities.

That’s right. Just because your shit is on the blockchain, that doesn’t

mean you get to solicit your fucking Ponzi scheme to people in America.

State regulators will have something to say about that.

Via the company’s website, as per the reasons for shutting down.

The reason for halt of lending and exchange platform has many reasons as follow:

The continuous bad press has made community members uneasy and created a lack of confidence in the platform.

We have received two Cease and Desist letters, one from the Texas State

Securities Board, and one from the North Carolina Secretary of State

Securities Division. These actions have become a hindrance for the legal

continuation of the platform.

Outside forces have performed DDos attacks on platform several times

and have made it clear that these will continue. These interruptions in

service have made the platform unstable and have created more panic

inside the community.

Price action.

What did Bitconnect do? They quite literally ran a Ponzi scheme. Look

at one of their brochures, promising investors 40% returns, PER MONTH.

Via Tech Crunch:

Many in the cryptocurrency community have openly accused

Bitconnnect of running a Ponzi scheme, including Ethereum founder

Vitalik Buterin.

The platform was powered by a token called BCC (not to be confused

with BCH, or Bitcoin Cash), which is essentially useless now that the

trading platform has shut down. In the last The token has plummeted more

than 80% to about $37, down from over $200 just a few hours ago.

If you aren’t familiar with the platform, Bitconnect was an

anonymously-run site where users could loan their cryptocurrency to the

company in exchange for outsized returns depending on how long the loan

was for. For example, a $10,000 loan for 180 days would purportedly give

you ~40% returns each month, with a .20% daily bonus.

Bitconnect also had a thriving multi-level referral feature, which

also made it somewhat akin to a pyramid scheme with thousands of social

media users trying to drive signups using their referral code.

The platform said it generated returns for users using Bitconnnect’s

trading bot and “volatility trading software”, which usually averaged

around 1% per day.

Of course profiting from market fluctuations and volatility is a

legitimate trading strategy, and one used by many hedge funds and

institutional traders. But Bitconnect’s promise (and payment) of

outsized and guaranteed returns led many to believe it was a ponzi

scheme that was paying out existing loan interest with newly pledged

loans.

The requirement of having BCC to participate in the lending program

led to a natural spike in demand (and price) of BCC. In less than a year

the currency went from being worth less than a dollar (with a market

cap in the millions) to a all-time high of ~$430.00 with a market cap

above $2.6B.

Lenders into the Bitconnect Exchange have revealed the company is

closing out accounts, issuing BCC in exchange for their dollars — which

is causing the price to plummet.

Bitconnect is officially closing up. They sent me

33 BCC for my $11k+ in loans. Worth $6600 and dropping by the second.

Their exchange is down so the only option is to send the BCC to an

external exchange.

Free To A Good Home

-

I know what gooning is same as I know what felching is but I don't care to

remind myself all that often about it. The Internet just keeps exposing the

ni...

If Free Will Is False, Destiny Is True

-

Free will is like God: perhaps dead, its absence having something to say

about morality (what Nietzsche meant by “Gott ist tot” was that the

Christian God ...

FREE BOOK: On Nonviolence

-

“Michael Barker’s interrogation of nonviolent protest tactics and regime

change is both timely and important. Drawing on cases ranging from American

democr...

Return of the Magi

-

Lately, the Holy Spirit is in the air. Emotional energy is swirling out of

the earth.I can feel it bubbling up, effervescing and evaporating around

us, s...

Covid-19 Preys Upon The Elderly And The Obese

-

sciencemag | This spring, after days of flulike symptoms and fever, a man

arrived at the emergency room at the University of Vermont Medical Center.

He ...

-

(Damn, has it been THAT long? I don't even know which prompts to use to

post this)

SeeNew

Can't get on your site because you've gone 'invite only'?

Man, ...

First Member of Chumph Cartel Goes to Jail

-

With the profligate racism of the Chumph Cartel, I don’t imagine any of

them convicted and jailed is going to do too much better than your run of

the mill ...